Emotional Triggers and Self Control in Financial Submission: How to Recognize, Respond, and Protect Yourself

Emotional triggers and self control in financial submission interact in ways that surprise most people. They are not only about temptation or greed. They are about attachment, meaning, shame, and identity. I will walk through what I see repeatedly, share subtle examples from real situations, and suggest practical steps that respect personal autonomy while reducing harm.

Why emotions matter more than budgets

When I talk to people who have lost control of financial boundaries in submissive relationships, the common thread is an emotional flashpoint. A message that flatters, a crisis that asks for help, or the simple approval from a dominant can catalyze a pattern of giving that money rules alone seldom stop.

Money acts as language. It signals care, loyalty, and status. That meaning is cheap when you ignore the emotional economy behind the exchange. I often point people to resources about finding responsible guidance , for example, how to find a findomme if you are exploring a dynamic but want safer, informed choices.

Common emotional triggers in financial submission

- Approval and praise: A compliment from a dominant can feel like oxygen and can override previously set limits.

- Fear of abandonment: Small gifts or steady contributions become a perceived insurance policy against rejection.

- Ritual and identity: Regular payments can become rituals that cement identity and make stopping feel like losing self.

- Crises and emergencies: Requests framed as urgent tend to short-circuit deliberation and increase impulsive giving.

How self control actually fails

Self control is not a single muscle that either works or doesn’t. It is a set of processes: attention, emotion regulation, future planning. Stress, sleep loss, alcohol, or even a private shame loop can weaken any of those processes for a day or longer. In practice I see two failure modes most often:

- Escalation: Small gifts escalate as the giver seeks the same emotional return. The feeling that “this time will be different” cuts in later.

- Narrowing of options: When emotion narrows thinking, people stop considering alternatives like pausing, asking for verification, or getting a second opinion.

These dynamics help explain why spreadsheets and rules are helpful but often insufficient.

Real-life examples

Example 1: A man I spoke with described paying for month-to-month luxuries after a breakup. He told himself the payments kept him connected. On his good days he would have said no. But at night, alone and anxious, he gave repeatedly. The payments were less about the recipient and more about soothing a fear of being forgotten.

Example 2: A woman set a monthly cap and used an app to alert her. When she received an unexpected late-night DM that threatened to end the relationship unless she sent an immediate gift, she ignored the app and sent double. Afterwards she admitted she reacted to the threat of loss more than to any rational calculation.

Practical strategies that actually work

- Design in friction. I recommend cooling-off tools: delays, third-party approval, or requiring a simple action that breaks the emotional surge.

- Change the reward structure. Replace instant emotional relief with predictable, non-financial rituals: regular video calls, time-limited treats, or non-monetary tributes.

- Externalize accountability. I have seen the combination of a trusted friend and a written commitment reduce impulsive transfers far more than budgeting apps alone.

- Test commitments in low-stakes ways. Try a temporary pause and observe how your anxiety and sense of identity shift over weeks, not hours.

When exploring options or safer practices I often refer to community advice and model resources like discussions about findom and committed relationships to see how others balance intimacy and money.

Trade offs and tensions

Any control strategy changes the dynamic. More friction can feel cold and reduce intimacy. Less friction preserves spontaneity but increases risk. There is no perfect balance. I encourage testing small changes and noting emotional responses as data, not failure.

There is also the tension between autonomy and protection. Overly paternalistic rules can undermine agency. Yet doing nothing can lead to harm. My approach is to preserve agency while creating structures that make harm less likely.

Legal and practical safety steps

- Keep separate bank accounts and set firm transfer limits you cannot easily override without a cooling period.

- Document requests that feel urgent. A pattern of manipulative pressure is often visible only in records.

- Seek impartial financial advice when large sums are involved. An outside perspective catches patterns emotion misses.

For people actively involved in online financial dynamics, practical guides and warnings can help avoid predictable pitfalls. I recommend reading issues and warnings tailored to paypigs and financial submissives, such as practical warnings for paypigs.

When therapy can help

Therapy is useful when patterns repeat despite protections. I do not mean immediate pathologizing. Rather, therapy helps unpack why certain triggers are so persuasive: childhood attachments, shame, or unprocessed losses often show up as financial behavior.

Even a few sessions focused on impulse control and boundary practice can change how you respond in the moment.

Balancing honesty with boundary-setting

Communicating limits honestly is hard. People fear disappointing a dominant or appearing weak. I suggest short, factual scripts that state the boundary and the reason. For instance: “I have a rule to pause on gifts over X. I need to keep it.” This reduces bargaining and keeps you accountable to yourself.

If you are learning how to navigate these conversations, community advice for models and protocols can be helpful. See a concise roundup of model resources at financial domination resources for models.

Final thoughts

Emotional triggers and self control in financial submission are not moral failings. They are predictable psychological dynamics. The goal is not to eliminate emotion but to design a life where emotion and money do not create repeated harm. Small structural changes, honest scripts, and outside accountability can change outcomes more reliably than willpower alone.

I tend to trust the quieter signals with emotional triggers and self control in financial submission. If the setup only works when you move fast or stop asking basic questions, that usually tells you more than the sales pitch does.

FAQ

- Q: Can someone be both autonomous and financially submissive safely?

A: Yes, when there are transparent agreements, cooling mechanisms, and outside accountability. Autonomy means you choose the structure that includes protections.

- Q: How do I tell if a request is manipulative?

A: Look for repeated urgency, threats of abandonment, or pressure that bypasses normal negotiation. If you feel rushed into a decision you normally would delay, that is a red flag.

- Q: Should I cut contact if boundaries are ignored?

A: Not always, but repeated disregard for clear limits is serious. I advise escalating protections: set technical limits, pause transfers, and seek external advice before resuming contact.

If you want a lighthearted perspective on resolutions and commitments for people who identify as paypigs, there are practical ideas in <

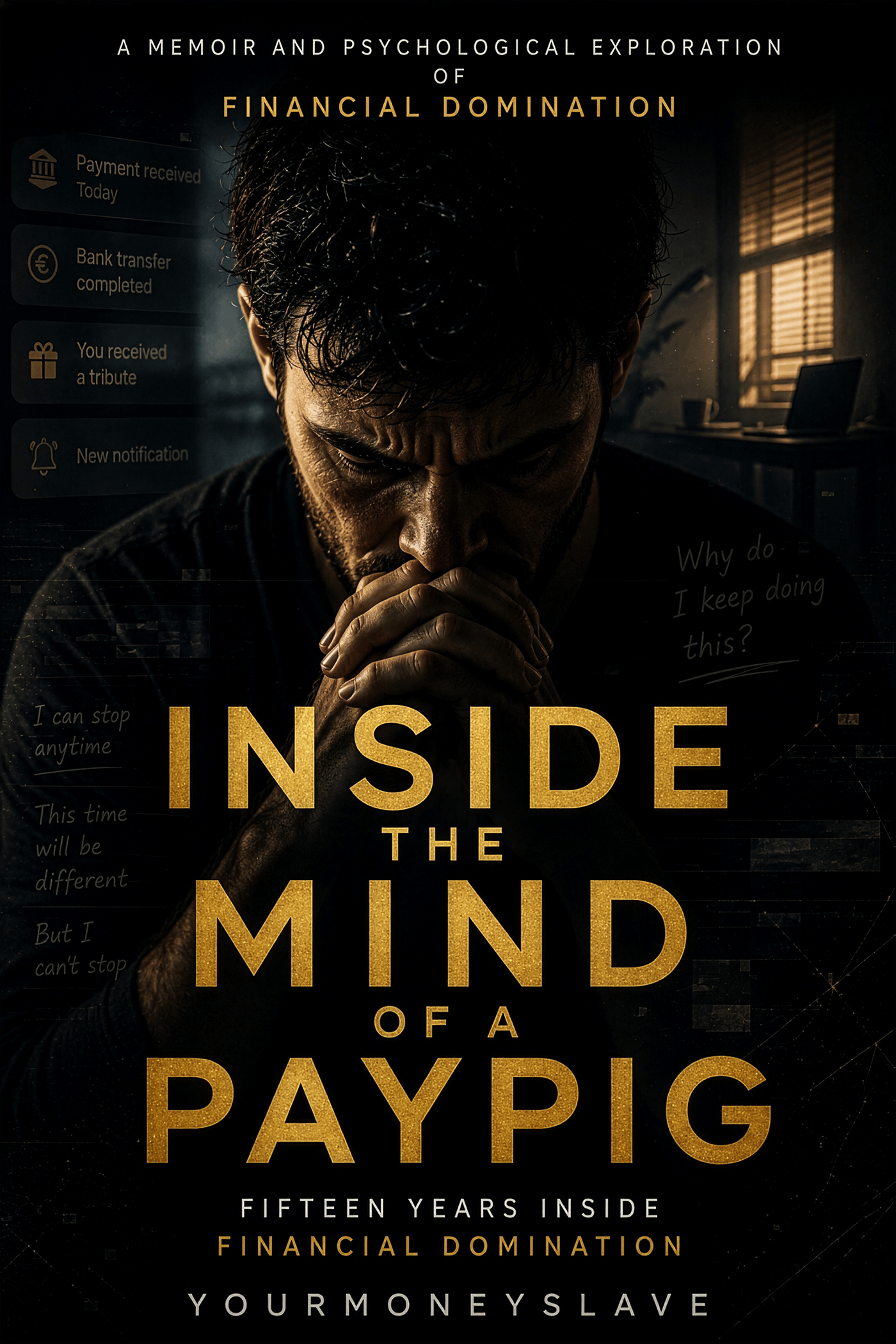

Inside The Mind Of A PayPig

After 15+ years inside financial domination, I finally wrote a book about obsession, shame, desire and the questions I am still trying to answer.

Read the free sample